-

Content

Customers love your product. They adore your service. They compliment your website but the moment they see the price tag, their smile can perform a full backflip into a frown. Here’s the good news: an installment payment option fixes that.

Here’s the better news: when customers see installment payments, they think, “Oh! This is actually doable.”

And here’s the very best news: you make more money without changing a single thing you sell.

And if you think installment payments are just a trend, think again. In 2024 alone, 86.5 million Americans used Buy Now, Pay Later (BNPL)— a form of short-term installment payments. That’s not niche. If you see names like Affirm or Klarna, that’s BNPL, that’s an installment payment plan in action and it’s “on every checkout menu” mainstream.

So let’s break down what installment payment plans actually are, how they help, and whether your business should offer them (spoiler: probably yes).

What is an installment payment plan?

An installment payment plan lets customers split a purchase into smaller, scheduled payments over time. It’s basically the financial version of eating a pizza one slice at a time instead of trying to fit the whole thing in your mouth at once. Instead of paying the full amount upfront, customers spread the cost out—weekly, monthly, bi-weekly, or whatever schedule fits your business. For merchants, installment payments can:

- Lower price resistance

- Increase conversions

- Reduce abandoned carts

- Turn “maybe later” into “okay, let’s do it!”

It’s affordability without the stress—for them and for you.

Types of installment payment terms

Not all installment plans are created equal. Some are simple. Some are spicy. Some are for people who alphabetize their pantry. Here are the most common versions:

Fixed installments

A predictable schedule with the same amount every billing cycle. Simple. Clean. Your accounting team’s favorite child.

Pay-in-3 / Pay-in-4 / Pay-in-6 months

The BNPL classics are usually provided by companies like Klarna or Affirm. Your customer’s credit card bank also could offer this with their own installment programs.

Custom intervals

Weekly, bi-weekly, semi-monthly, monthly—whatever matches customer budgets or your workflow.

Down payment + smaller installments

Ideal for services, custom orders, or higher-ticket items that need upfront commitment.

How do installment payments work?

Installment payments are straightforward once you break them down. Here’s the quick version of how they work from start to finish:

1. You and the customer agree on the service and the plan

Total amount, number of payments, billing schedule, and whether a deposit is required.

2. The customer pays a deposit (optional but helpful)

This locks in the purchase and gives your cash flow a boost before the work begins.

3. Payments are charged automatically on a schedule

Weekly, bi-weekly, monthly — whatever you set. Customers don’t need to remember anything.

4. Your payment provider handles retries and reminders

With a provider like Helcim, failed payments retry automatically and notifications go out without you doing a thing.

5. Payments continue until the balance is fully paid

Once the last installment clears, the purchase is complete and the final invoice gets sent with the balance of zero.

Installment payments let your customers spread out the cost while still giving you predictable, timely revenue — especially when your provider automates the entire process.

How is an installment plan different from BNPL?

BNPL is technically an installment payment—just outsourced. Here’s the difference:

- BNPL is run by a third-party provider who pays you upfront, collects from the customer, and takes a cut.

- Merchant-run installment plans within your payment platform (if they support it) give you full control over terms, timelines, and fees.

Which businesses should offer installment payments?

Short answer: any business where customers hesitate at the price. Longer answer: many, many industries benefit from installment payments but it’s mostly useful for merchants with more than $200 worth of items.

Best-fit industries

- Retail & eCommerce

- Contractors & home services

- Professional services (dental, legal, coaching, consulting)

- Education & training

- B2B equipment or service providers

- Anyone invoicing clients

If your average sale is $200 or more, installment options can transform casual browsers into paying customers.

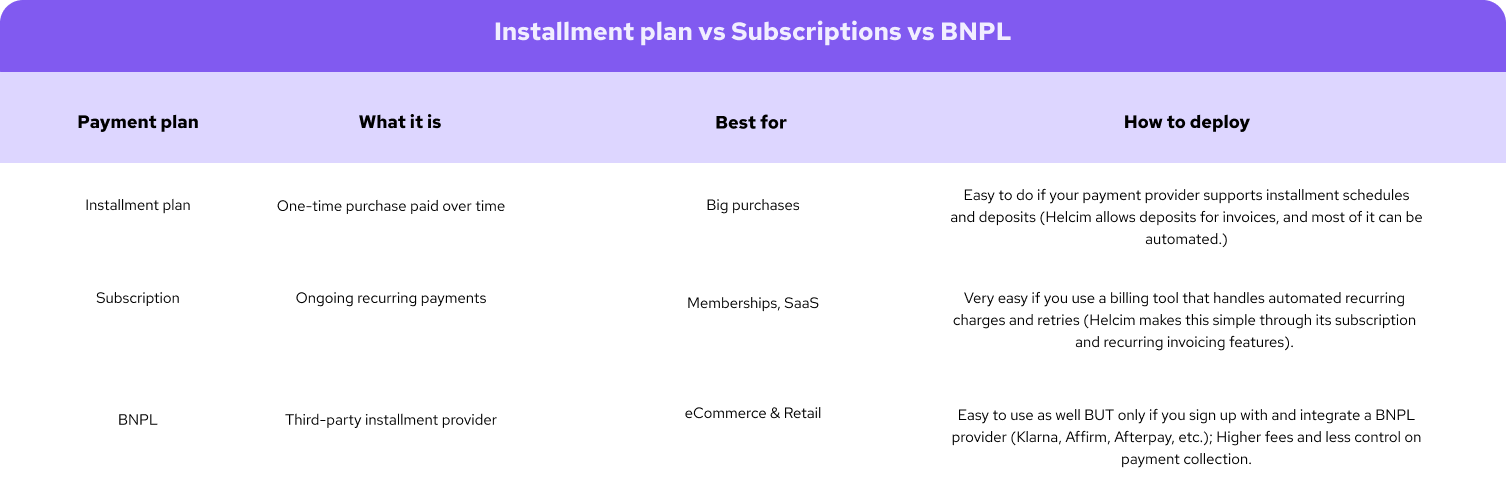

Installment plan vs Subscription vs BNPL

If the difference for installment payment plan, subscriptions, and BNPL is still muddy for you, here's a brief comparison to show which one would best certain scenarios for your business:

BNPL, again, is an installment plan—but the main difference is that this is run by a third-party.

What are the advantages of installment payments?

Installments lower the emotional temperature around pricing. Customers feel good buying from you—and that’s priceless.

Increase conversions

When customers don’t have to pay the full amount upfront, they’re far more likely to complete the purchase instead of hesitating or abandoning their cart. Flexible payments remove the biggest blocker: sticker shock.

Boost average order value

Customers are more open to upgrades, higher-tier packages, or add-ons when the total cost is split into smaller payments. Installments make “the nicer option” feel suddenly very reasonable.

Reduce cart abandonment

Price hesitation is a top reason customers leave at checkout. Offering installment payments removes that barrier and gives them a clear, comfortable path to saying yes.

Help you compete with brands offering flexible checkout

Big retailers and online marketplaces already offer multiple pay-over-time options. When you match that convenience, you stay competitive and prevent customers from defaulting to bigger brands.

Improve cash flow with deposits and partial payments

Accepting deposits or partial payments upfront as part of an installment plan helps your business secure revenue before the work begins, which keeps cash flowing while reducing financial risk. Whether you're in services, trades, or project-based work, installment deposits ensure you’re not waiting until the end to get paid.

What are the disadvantages of installment payments? (because we’re honest here)

Not all installment payments are fail-proof, and some businesses may decide they’re not the right fit — and that’s okay. Still, it helps to understand the common challenges so you can plan for them.

Failed payments can happen

Even with automated retries, some customers will miss a payment or forget to update their card. It’s inconvenient, but manageable with a good system in place.

Cash flow can be slower unless your provider pays upfront

When payments are spread over time, you receive revenue more gradually. Some businesses don’t mind the steady stream, while others prefer full payment immediately.

Requires automation to avoid chaos

Trying to manage installment plans manually is how villains are born. You need a payment provider that can handle schedules, retries, and reminders automatically.

Customers occasionally overestimate their wallet strength

Flexible payments make larger purchases feel easier, but that sometimes leads to optimistic budgeting. Clear communication and reliable billing tools help reduce surprises.

All of these challenges are real — but most of them disappear with a provider that’s actually built to handle installment plans, recurring billing, and deposits properly.

What you need to accept installment payments

To offer installment plans without crying into your spreadsheets, you’ll need:

- A payment provider that supports deposits, installment schedules, or recurring payments

- The ability to store a customer’s card or bank account on file

- Automated reminders, retries, and payment logging

- An invoicing tool that can handle deposits or partial payments

- Clear customer terms

If your payment processor already includes these features (for example, Helcim supports recurring billing, deposits, automated retries, and recurring invoices), you're basically set. You choose the payment plan, send the invoice or checkout, and the system handles the awkward follow-ups for you.

Should your business offer installment plans?

Ask yourself:

- Do customers hesitate at your price?

- Do you sell anything over $200?

- Do you want higher conversions?

- Do competitors offer flexible payments?

- Do you enjoy revenue? (trick question)

If you answered yes to any of these, installment plans belong in your business.

How Helcim can help

If you’re not quite ready to jump into a full BNPL integration (totally fair — commitment is hard), you can still offer flexible payments using recurring billing or recurring invoices. Helcim makes this part easy — you can:

- Create subscription plans or recurring invoices with custom billing cycles

- Automatically retry failed payments

- Send recurring invoices for customers who prefer paying through an invoice

- Track everything inside your merchant dashboard

- Offer multiple ways to pay whether it’s through credit card payments or ACH payments

- Request a deposit and take partial payment toward the remaining balance

So instead of manually re-billing, re-invoicing, or re-reminding (unquestionably the three worst “re-” words), the system just handles it for you.

If you want to try installment-style billing without extra fees or complicated setup, you can get started today by creating a free Helcim account. It’s straightforward, flexible, and — best of all — no limiting contracts!

Frequently asked questions

What happens if a customer can’t make an installment payment?

With most providers—and typically with Helcim—the system will automatically retry the payment to give the customer a chance to resolve the issue. If it still fails, both the merchant and the customer are notified so the billing information can be updated or the payment plan can be adjusted or paused as needed.

What should you do if a customer’s card declines?

Retry the payment first, then request an updated card or offer ACH as an alternative. If it still doesn’t go through, a provider with built-in notifications—like Helcim—will alert the customer automatically, and you can temporarily pause service until their billing information is updated.

Can installment terms be changed mid-plan?

As long as both parties agree and the original terms allow for adjustments, you can update the payment schedule or amounts without interrupting the plan.

Can customers pay their installment plan early?

Absolutely — most systems allow customers to pay off their remaining balance at any time. Early payments are a win-win: merchants get paid sooner, and customers often avoid additional fees or interest.

Do installment plans charge interest?

Merchant-run installment payments typically don’t include interest, while BNPL providers may charge interest depending on the plan and risk profile. Pay-in-4 options are usually interest-free, but it ultimately depends on the provider and the specific terms you choose.