-

Content

Last Updated on July 11, 2025 by Robert Luong

Running a business is incredibly rewarding, but it is challenging, especially about managing your finances. Knowing how money moves in and out of your business, and which payment methods to use, is important to keeping your business running smoothly.

Two terms that confuse business owners are EFT and ACH payments. They sound similar, but they’re not exactly the same. So is an ACH payment just another type of EFT? Or do they work differently?

To clear up the confusion, we’ll break down what each term means, how they work, and the key differences that matter for your business.

Is an EFT payment the same as an ACH payment?

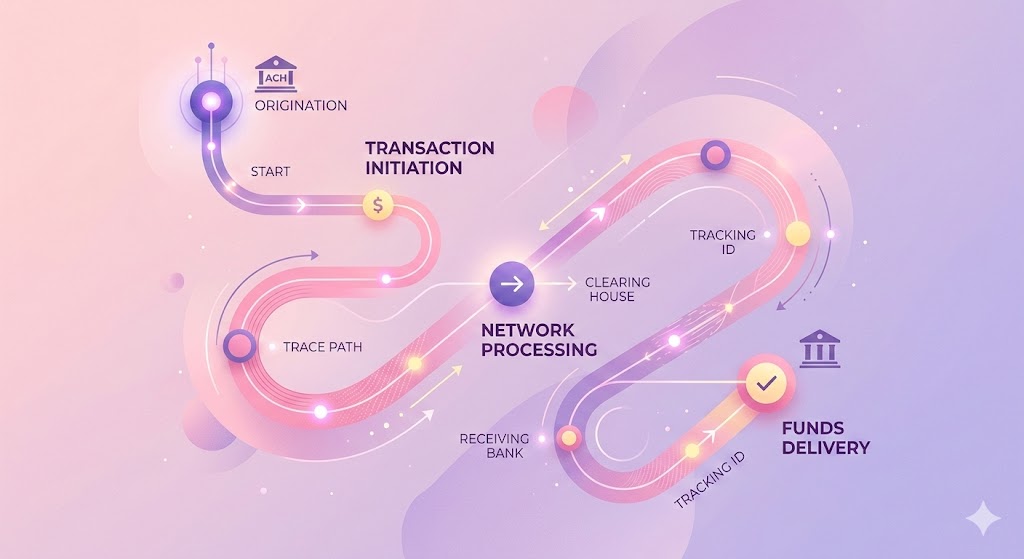

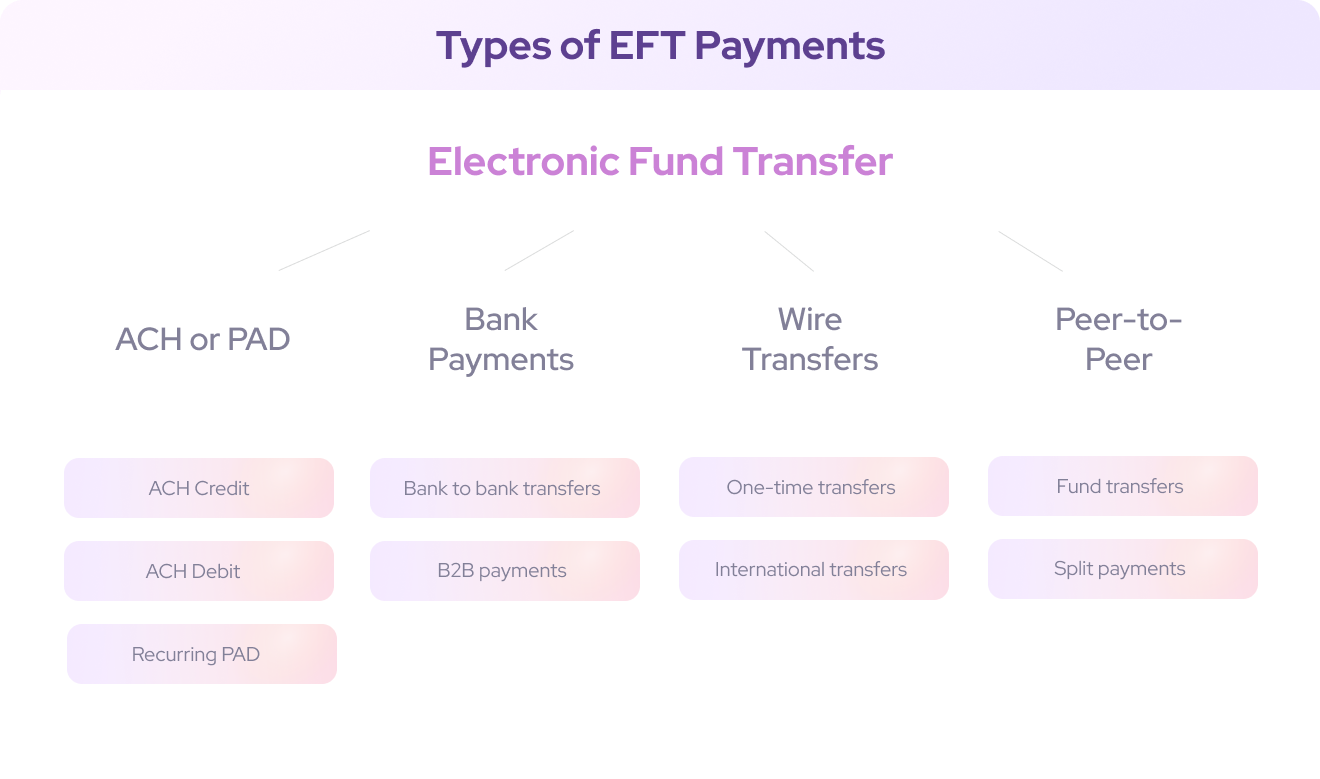

EFT (electronic funds transfer) covers all electronic ways to move money, such as ACH, credit card, debit card, or wire transfers. ACH (Automated Clearing House) is a type of EFT used in the United States and is regulated by NACHA. ACH network connects banks and credit unions across the U.S. so they can process electronic payments and handle settlements.

In Canada, businesses often use PADs (Pre-authorized Debits), also known as Canadian EFT, which is similar to ACH transfers in the U.S.

Which is better for large transactions: ACH or EFT payments?

If your business processes high payment volume, ACH payments are built for this. The ACH network was designed to handle massive volumes of transactions across the U.S. In the first quarter of 2025 alone, NACHA reported that ACH payment volume rose 4.2% to 8.5 billion transactions, with a total value of $22.1 trillion, up $1.4 trillion (6.6%) from a year earlier.

EFT includes ACH along with other electronic payment methods like wire transfers, debit card transactions, and credit card payments. Other EFT methods don’t scale as well as ACH. For example:

- Wire transfers are fast but expensive, and not practical for paying 5,000 vendors at once (learn more about how ACH payment compares to wire transfer).

- Credit card payments work well for consumer purchases but get expensive for large B2B payouts, often around 2.5% compared to about 0.5% for ACH (learn more about how ACH payment compares to credit card).

- Debit cards used online usually run through credit card networks, costing as much as credit cards.

If your business is growing and needs to handle a high volume of transactions without costs ballooning, ACH is generally the better tool under the EFT umbrella.

What are the typical processing times for ACH and EFT payments?

Canadian EFT (PAD) and ACH transfers usually take 3 to 5 business days. Other EFT payment methods are faster:

- Wire transfers are typically the fastest, often clearing the same day or even within a few hours, but they cost more.

- Debit or credit card transactions usually settle within 1 to 2 days on the back end.

- Electronic checks (eChecks) can take 1 to 2 business days.

ACH is slower than other EFT payments like debit or credit cards because the payments have to go through multiple financial institutions to settle in your account. Some payment providers offer same date ACH payments, but that often comes with extra fees such as 1.5% transaction amount.

What are the advantages and disadvantages of ACH vs. EFT payments?

1. Advantages of ACH and Canadian EFT (PAD)

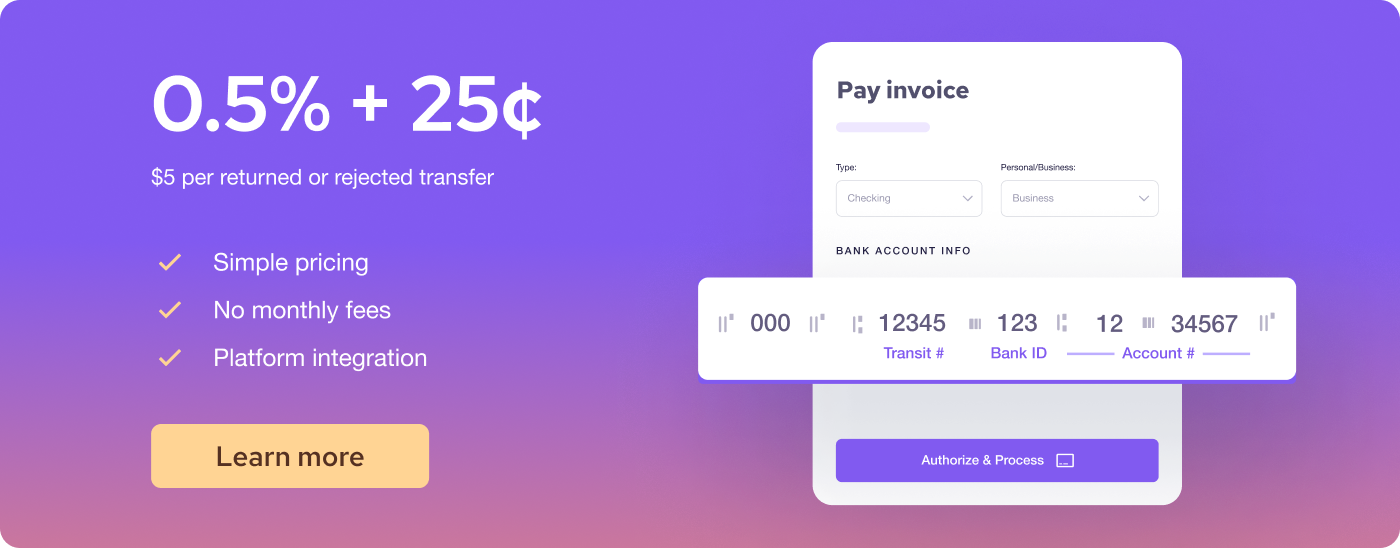

ACH payments and PAD are far more affordable than most other types of EFT payments. For example, Helcim charges just 0.5% + 25¢ per ACH or PAD transaction, and caps the fee at $6 for payments under $25,000. This makes a huge difference if you’re processing large invoices or payroll.

Compare that to other EFT digital payment methods:

- Debit card processing fees: 1% to 2.5% per transaction

- Credit card processing fees: 2% to 3% per transaction

- Wire transfer processing fees: $10 to over $50 per transaction

- Check processing fees: $10 or more per check, depending on the banks and the check amount

However, other EFT payments are faster than ACH payments.

2. Disadvantages of ACH and Canadian EFT (PAD)

Longer processing times: ACH and PAD payments generally take 3 to 5 business days to clear. If you’re counting on instant cash flow, ACH/PAD may delay your cash flow. Many businesses plan around this by keeping a cash buffer in their accounts. Some only use ACH or PAD for predictable recurring payments like monthly recurring invoices, installment plans, or subscriptions.

ACH/PAD dispute risks: Customers can dispute ACH or PAD debits. In Canada, they have up to 90 days (or even 1 year in some cases) to claim a debit wasn’t authorized. In the U.S., if you can’t produce proof of authorization quickly, the payment can be reversed. To mitigate this risk, you should keep all authorization forms organized, so if there’s ever a dispute, you can prove the payment was approved (learn how to handle ACH dispute).

Higher risk of insufficient funds: ACH and PAD pull money directly from the customers’ banks. So, if they don’t have enough money in their account, the transaction fails. To navigate this risk, you can schedule payments on days when their customers are likely to have funds (like after payday).

Limited international transactions: ACH is strictly a U.S. network, and Canadian EFT is built for Canadian merchants. If you want to pay or get paid internationally, you’d have to look at wire transfers or other cross-border EFT solutions.

Are there any legal or regulatory requirements for using ACH and EFT payments?

Yes, merchants must comply with several legal and regulatory requirements when using ACH (U.S.) and EFT or PAD payments (Canada). Here's what you need to know:

U.S. ACH Payment Requirements:

- Merchants must obtain clear, written, or electronic NACHA-compliant authorization forms with detailed payment amounts, frequency, and how customers can cancel.

- Merchants must provide customers with a copy of the authorization form or terms.

- Keep records of ACH authorizations for at least two years from the date of the last transaction.

- Be ready to provide authorization records if a customer disputes an ACH payment (learn how to handle ACH dispute)

- Customers must be able to revoke their authorization easily, and merchants must clearly explain how to do this.

- Merchants must notify customers in advance (at least 10 days) if ACH payment amounts or dates change.

- Keep your unauthorized return rate under 0.5% to avoid fines or restrictions from NACHA.

Canadian EFT (PAD) Payment Requirements:

- Have a signed PAD (Pre-Authorized Debit) agreement from each customer, clearly stating payment amount, timing, and cancellation terms.

- Clearly outline cancellation procedures and timelines (maximum notice period is 30 days).

- Provide customers with a written copy or confirmation of the PAD agreement at least 10 days before the first payment (customers can waive this requirement to receive confirmation within 5 days after the first debit).

- Customers can dispute unauthorized debits within 90 days (or up to 1 year in certain cases).

- If a PAD payment isn't consistent with the agreement terms, customers have the right to reimbursement.

What types of businesses commonly use ACH payments and Canadian EFT (PAD)?

ACH in the U.S. and PAD in Canada are popular with businesses that want to save on processing fees or keep cash flow steady. It’s especially valuable for companies with repeat customers or long-term contracts, where setting up an automatic electronic bank transfer just makes sense.

Below are some examples of businesses that commonly use ACH and PAD:

- Subscription services: Gyms, Saas companies, and membership businesses use ACH or PAD to collect monthly fees directly from customers’ bank accounts.

- Professional services: Accountants, lawyers, and consultants often collect invoice payments using ACH or PAD to avoid expensive credit card processing fees.

- Wholesale and B2B suppliers: Businesses paying for large orders typically prefer ACH or PAD to minimize the payment processing fees.

- Property managers and landlords: Tenants can set up automatic payments to pay rent each month.

- Utility and telecom providers: Many providers let customers fill out an online authorization form that gives them permission to automatically withdraw payments each billing cycle.

What are the transaction limits for ACH and EFT payments?

ACH transaction limits: NACHA currently sets a maximum of $1 million per ACH payment, effective as of 2022. For regular (non-same-day) ACH payments, there’s technically no universal maximum.

Canadian EFT (PAD) limits: In Canada, there’s generally no fixed maximum set by Payments Canada for PADs. Instead, the limits are typically determined by your bank or payment processor’s own risk policies.

What are the transaction limits for other EFT payment methods?

- Credit cards: Transaction limits for credit cards depend entirely on your customer’s available credit. If the purchase amount is higher than their credit line or remaining balance, the payment is declined. Some customers also place their own per-transaction caps for extra security.

- Debit cards: Debit card payments are limited by the funds your customer has in their checking account, plus any daily or per-transaction spending limits set by their bank.

- Contactless credit and debit card payment: If your customers pay by tapping their credit or debit card, there’s also a separate limit for contactless transactions. This is typically set between $250 and $500 per tap, depending on the card and the bank.

- Wire transfers: Wires are often used for very large payments because they generally have no formal ceilings. Banks do monitor large wires for compliance, but they rarely impose hard caps.

- eChecks: An eCheck works like a digital version of a paper check, processed through ACH in the U.S. or EFT in Canada. They typically follow the same transaction flexibility as ACH or PAD.

Keep in mind: No matter the method, your payment processor or bank can set their own transaction caps. They look at your business’s risk profile, transaction history, and industry to decide how high those limits can go.

How secure is ACH compared to other EFT payment methods?

When it comes to security, ACH and Canadian EFT (PAD) payments are among the most regulated forms of electronic payments.

- In the U.S., Nacha’s Operating Rules require payment processors to keep customer bank data encrypted (minimum 128-bit SSL) when it’s transmitted or stored.

- In Canada, Payments Canada’s rules require merchants to use “commercially reasonable” methods to verify a customer’s identity and account info before processing PAD payments.

Are Canadian EFT (PAD) and ACH payments more secure than other EFT options like wire transfers or credit cards?

- Wire transfers are also processed directly by banks, but if fraudsters or scammers trick customers into wiring money, it’s almost impossible to reverse (learn more about how to prevent ACH frauds here).

- Credit card payments follow strict PCI DSS requirements, but fraudsters can exploit credit card chargebacks to get products without paying. Plus, credit card skimmers can steal card data the moment customers insert or swipe their cards.

Start accepting Canadian EFT (PAD) and ACH payments with Helcim

Whether you choose ACH transfers or Canadian EFT (PAD), Helcim lets you accept both at a low processing cost: 0.5% + 25¢, capped at $6 for transactions under $25,000.

Not only that, Helcim also provides a suite of free tools to help you take ACH and EFT payments. There are no monthly fees, contracts, or hidden charges, you only pay the processing cost when a transaction is successfully completed.

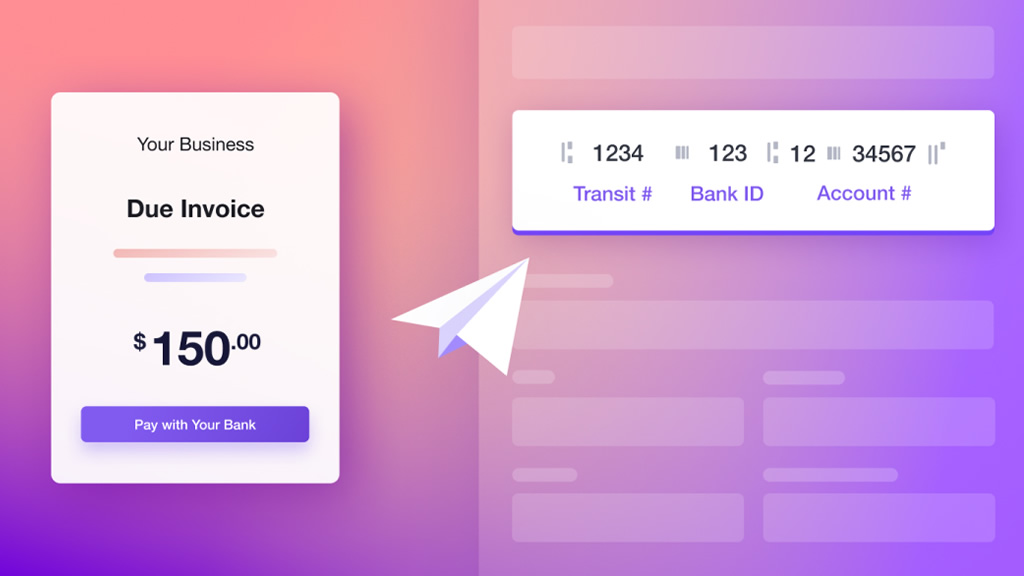

- Helcim Virtual Terminal: Process EFT and ACH payments online without any hardware, from your laptop, tablet or mobile.

- Helcim Invoicing: Send online invoices, handle late payments and automate follow-ups.

- Helcim Recurring Payments: Automate billing, customize subscription plans, and grow revenue effortlessly.

- Helcim Payment Pages: Securely add payment functionality to your website, with no programming required.

FAQ

Which is better for recurring payments: ACH or EFT?

ACH electronic transfers and Canadian EFT (PAD) are both excellent for recurring payments. Once your customers sign the authorization form, payments are automatically collected and deposited into your bank account. The processing costs are also lower than credit cards, so you keep more revenue in the long run. If you’re in the U.S., ACH is your best bet; in Canada, PAD is the standard.

Is ACH or EFT cheaper for small businesses?

ACH payments and Canadian EFT (PAD) are the most affordable ways to get paid, typically costing 0.5% + 25¢ per transaction, with fees capped at $6 for payments under $25,000. Other EFT options like credit cards, debit cards, or wire transfers are more expensive, with processing costs ranging from 1% to 3%.

What security measures are in place for ACH and EFT payments?

Both ACH and Canadian EFT payments follow strict data protection rules. In the U.S., Nacha requires encryption and fraud detection for ACH transactions. In Canada, Payments Canada requires merchants to use “commercially reasonable” methods to verify customers. Plus, customers must sign an authorization form, adding another layer of security that makes ACH and Canadian EFT very safe compared to many other payment methods.

What fraud risks come with ACH and EFT payments?

The biggest risks are unauthorized transactions or fraudsters providing fake bank account information. That’s why it’s critical for merchants to keep signed authorization forms on file, so they can prove ACH/EFT transactions were legitimate if disputes or fraud occur.

Can you use ACH or EFT for international payments?

No. ACH payments are limited to the U.S., and Canadian EFT (PAD) is mainly for domestic transactions. For international payments, businesses typically rely on wire transfers or specialized cross-border EFT services.

What are common myths about ACH and EFT payments?

Many believe ACH transfers and Canadian EFT (PAD) are slow and only for big companies, but small businesses use them daily for recurring transactions, installment plans, and subscriptions. Another myth is that they’re risky, when in reality they’re heavily regulated and often safer than checks or cards.

Is ACH or EFT better for large companies processing thousands of payments?

Yes. ACH and EFT can handle high volumes efficiently and keep costs far lower than credit cards or wires. That’s why large corporations use them for payroll direct deposit, supplier payments, and billing customers at scale.

Related Articles

-

How can I accept online ACH payments?

Ryleigh Stangness | August 29, 2023

-

What is an ACH return and how much does it cost?

Ryleigh Stangness | November 24, 2022

-

EFT VS Wire Transfers: What's the Difference?

Ryleigh Stangness | April 28, 2022

-

Welcome to Helcim ACH Payments

Danny Randell | March 15, 2022

-

What is an ACH transfer and how much does it cost?

Danny Randell | August 13, 2021